Clause 26-Section 43(B)

Clause 26-Section 43(B)

Section 43(B) of the income tax act provides a list of expenses allowed as deduction under the head ‘Income from business and profession’. It states some expenses that can be claimed as deduction from the business income only in the year of actual payment and not in the year when the liability to pay such expenses is incurred.

The following deductions are specified in this section

1. 43(B) (a) - Any tax, duty, cess, or fee paid under any law in force is allowed as a deduction when it is paid - this includes GST, customs duty, or any other taxes or cesses paid. Interest paid on these taxes is also eligible for deduction

2. 43(B) (b) - Contribution to any recognized employee’s benefit fund: contribution by the employer to any employee’s benefit fund namely PF fund, superannuation fund, gratuity fund before the due date for depositing those funds or before the due date of filing income tax returns

3. 43(B) (c) - Bonus or commission payable to employees - this amount should be the actual bonus/commission paid to employees and not dividends payable to them as shareholders.

4. 43(B)(d) - Interest on borrowings from Public Financial Institutions or State Financial Corporation in accordance with the conditions governing such loan.

5. 43(B)(e) - Interest on loans and advances from Scheduled Bank in accordance with the conditions governing such loan.

6. 43(B)(f) - Leave encashment provided by an employer to his employees.

7. 43(B)(g) - Payment to Indian Railways.

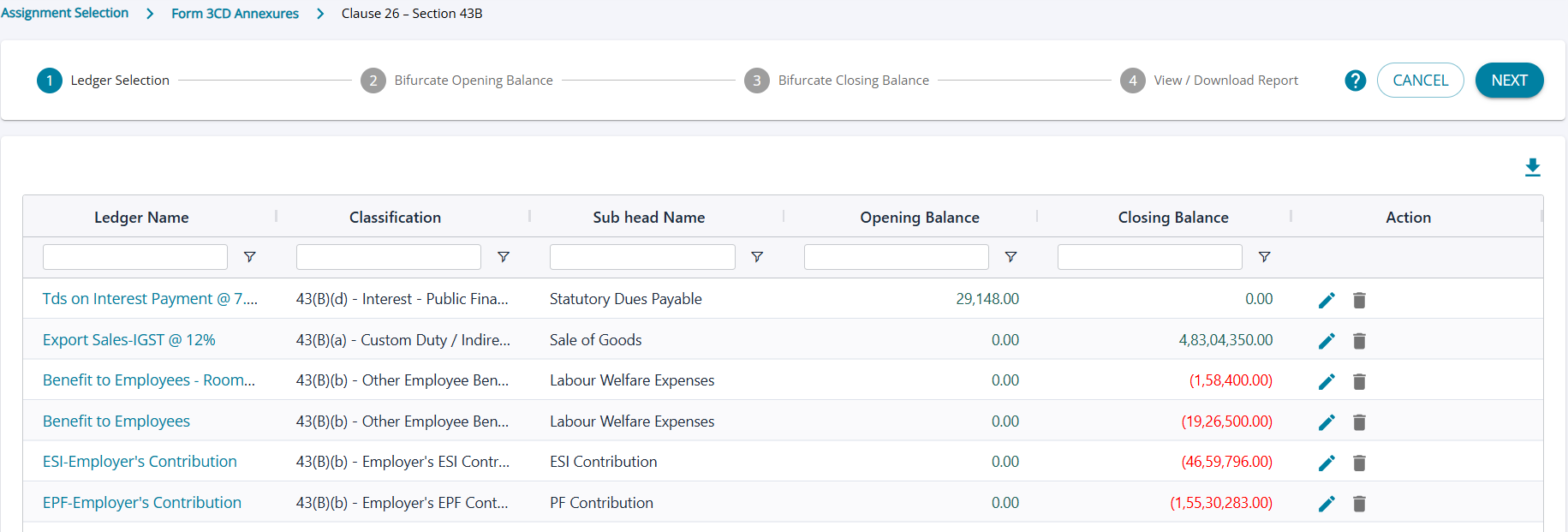

Step -1 - Ledger Selection

- Add the ledgers corresponding to PF / ESI payables, bonus and other statutory dues, as applicable to the client

- System does not pre-populate any ledgers for the client for year -1

- Classify the ledgers against 43(B) sub-clauses ( mandatory field for adding the ledger in step -1)

- If this information has been entered for the previous year, system will auto-populate the list with the same ledgers (if they are still valid ledgers as per current year's trial balance)

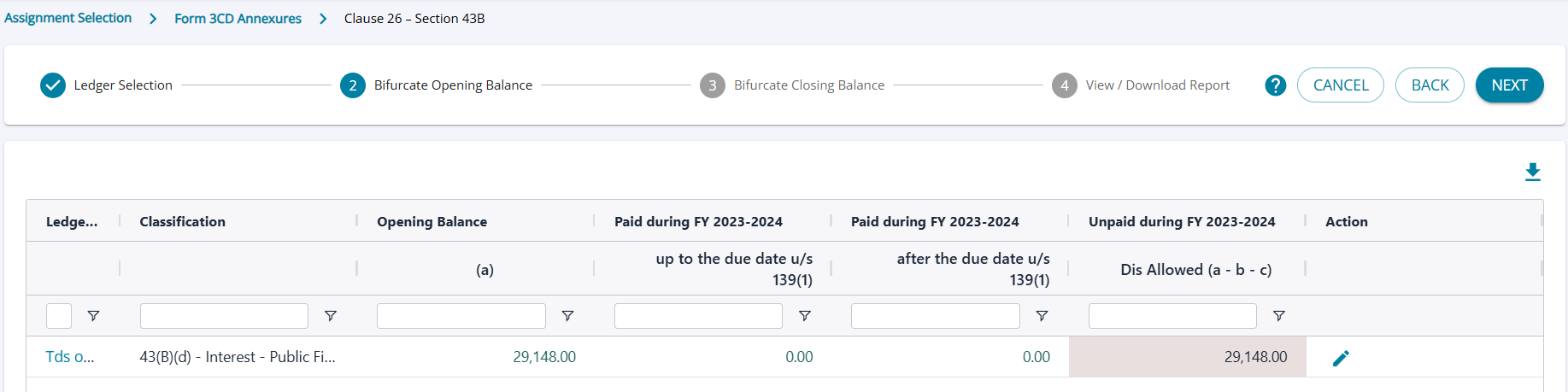

Step -2 : Bifurcation Opening Balance

1. Note: Only those ledgers having a credit Opening / Closing balance greater than zero as on 31st March shall be displayed in this step. Ledgers having:

(a) Debit Opening/ Closing balance, or

(b) Nil (Zero) Opening / Closing balance

shall not be displayed, as there is no outstanding liability requiring evaluation under Section 43B.

2. The user is allowed to provide bifurcation for the opening balance brought forward between:

(i) Paid During the FY (up to the due date u/s 139(1)) – Opening balance amounts that were paid on or before the due date u/s 139(1) of the earlier year and were therefore allowable and claimed as a deduction in that earlier year. These amounts are captured for reconciliation of the opening balance and do not result in any deduction in the year under audit.

(ii) Paid During the FY (after the due date u/s 139(1)) – Opening balance amounts that were paid during the year under audit after the due date u/s 139(1). These amounts were not eligible for deduction in the earlier year and may be considered for deduction in accordance with Section 43B in the year of payment.

The amount is captured in the report 26(i)(A)(a)

(iii) Unpaid & Disallowed – Opening balance amounts that continue to remain unpaid and therefore remain disallowable under Section 43B. Calculated field

The amount is captured in the report 26(i)(A)(b)

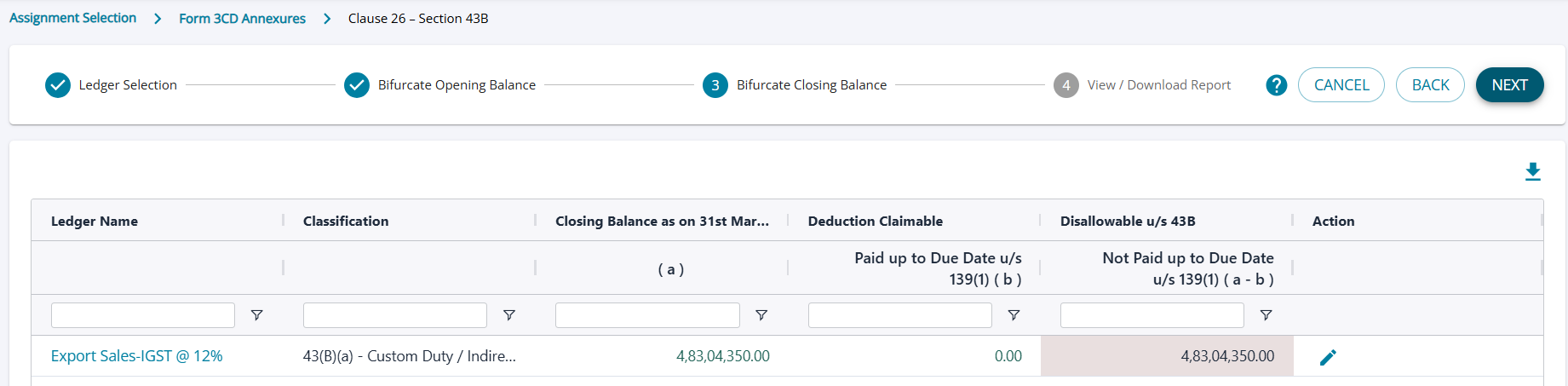

Step -3 : Bifurcate Closing Balance

For each selected ledger, the system automatically determines and populates the closing balance as on 31st March. The following columns are displayed:

(i) Closing Balance as on 31st March (a) - Liability outstanding as on the balance sheet date and covered under Section 43B.

(ii) Deduction Claimable - Paid up to Due Date u/s 139(1) (b) - Portion of the above closing balance that has been paid on or before the due date for filing the return of income under Section 139(1). This amount is allowable as a deduction.

(iii) Disallowable u/s 43B (Not Paid up to Due Date u/s 139(1)) (a-b) - Portion of the closing balance that remains unpaid as on the due date under Section 139(1). This amount is disallowable under Section 43B.

Note: Only those ledgers having a credit Opening / Closing balance greater than zero as on 31st March shall be displayed in this step. Ledgers having:

(a) Debit Opening/ Closing balance, or

(b) Nil (Zero) Opening / Closing balance

shall not be displayed, as there is no outstanding liability requiring evaluation under Section 43B.

Step -4 : View / Download Report

- The system provides 4 reports, one for each sub-clause of Clause 26 .

- The reports are available for excel export.