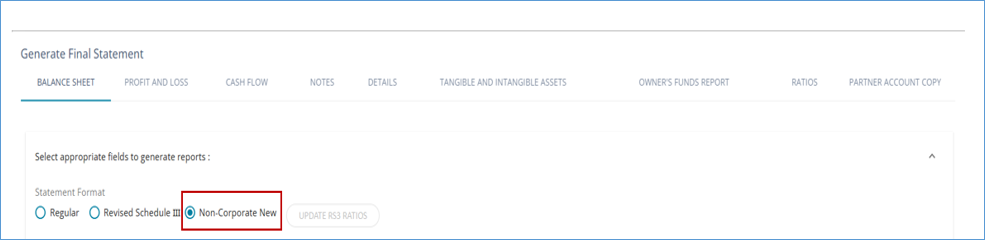

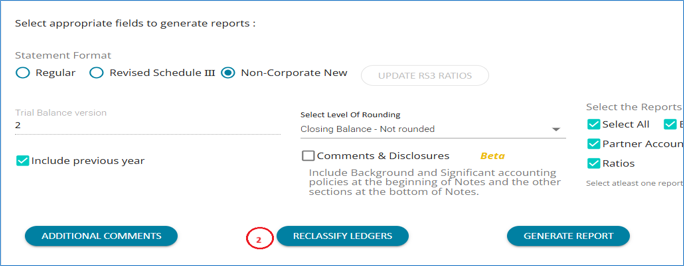

Statement Format - Non-Corporate New

The ICAI has issued a Guidance Note on Financial Statements of Non-Corporate Entities, which becomes applicable for financial statements covering periods beginning on or after 1st April 2024.

To align with this regulatory change, AssureAI has introduced a third option for financial statement generation — Non-Corporate New.

On the Client Setup screen, when the client’s status is any of the following, the Non-Corporate view will be auto-selected by default:

- Partnership Firms

- Association of Persons (AOP)

- Proprietorship (Individual)

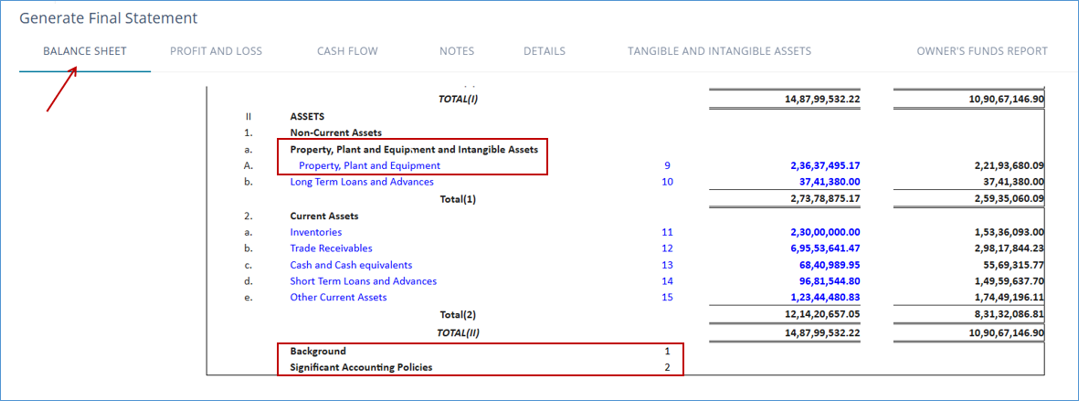

1.1 Changes to Balance Sheet

Under the "Assets" section of the balance sheet, Tangible and Intangible Assets are now displayed together under the consolidated sub-heading: "Property, Plant and Equipment and Intangible Assets".

The financial statements now include note numbers referencing key disclosures:

- Note 1: Background

- Note 2: Significant Accounting Policies

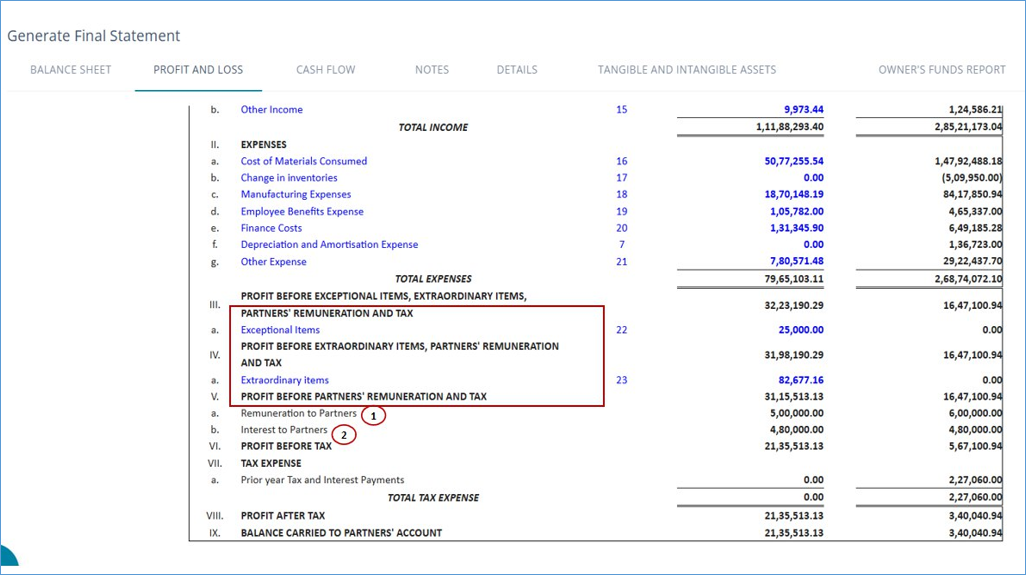

1.2 Changes to P&L Statement

- Rapped for this to take effect – elaborated on the next slide)

- Remuneration to Partners now moved above Tax expense

- Interest to Partners under Finance Cost (A new subhead has been created from the backend for your convenience - Ledgers have to be remunerable items displayed below Exceptional Items

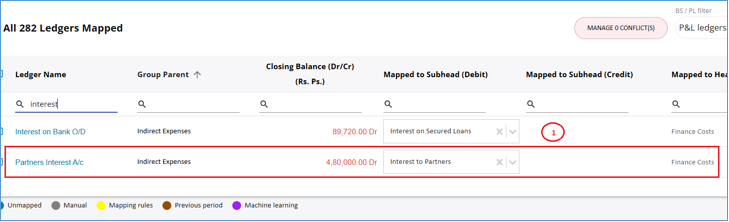

1.3 Note regarding “Interest to Partners”

- Previously, “Interest to Partners” was being shown under “Appropriations” on the face of the P&L statement

- As per the ICAI guidance note, this is to be grouped under Finance Costs

- Please follow the steps below to achieve this

Step 1: Map the current year ledger to “Interest to Partners” under Finance Cost.

Step 2: Use the “Reclassify ledgers” to map the previous year's ledger under the new subhead to show the comparatives. (This would be possible only if the ledger name has remained the same between the last year and the current year.)

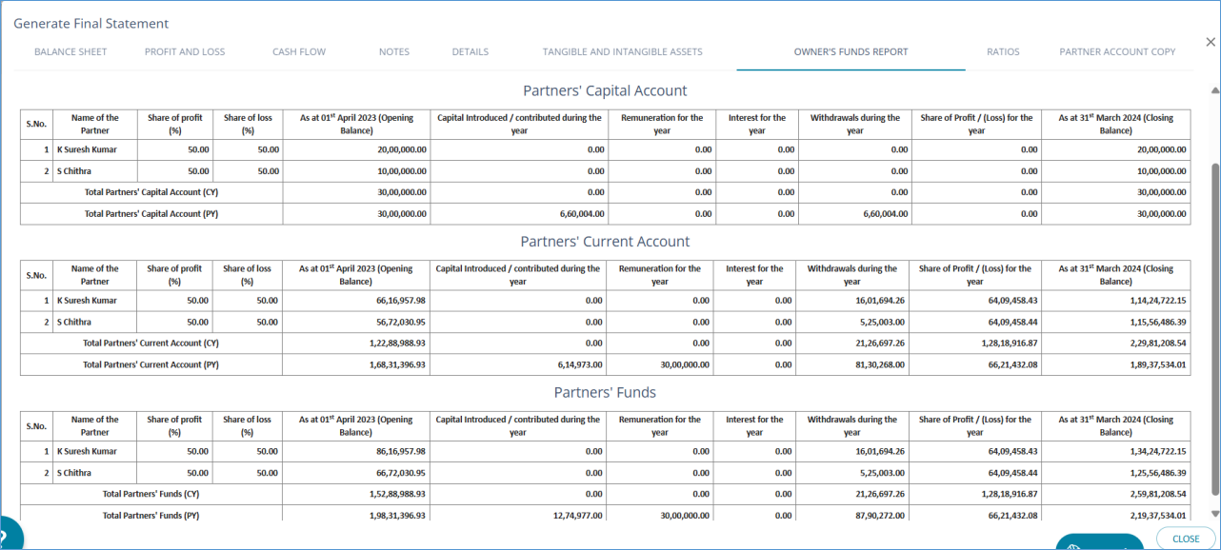

1.4 Changes to Notes

New Section: Owners’ Funds

This section summarizes the transactions in the partners’ or proprietor’s capital and current accounts, in the standard format as prescribed in the ICAI Guidance note.

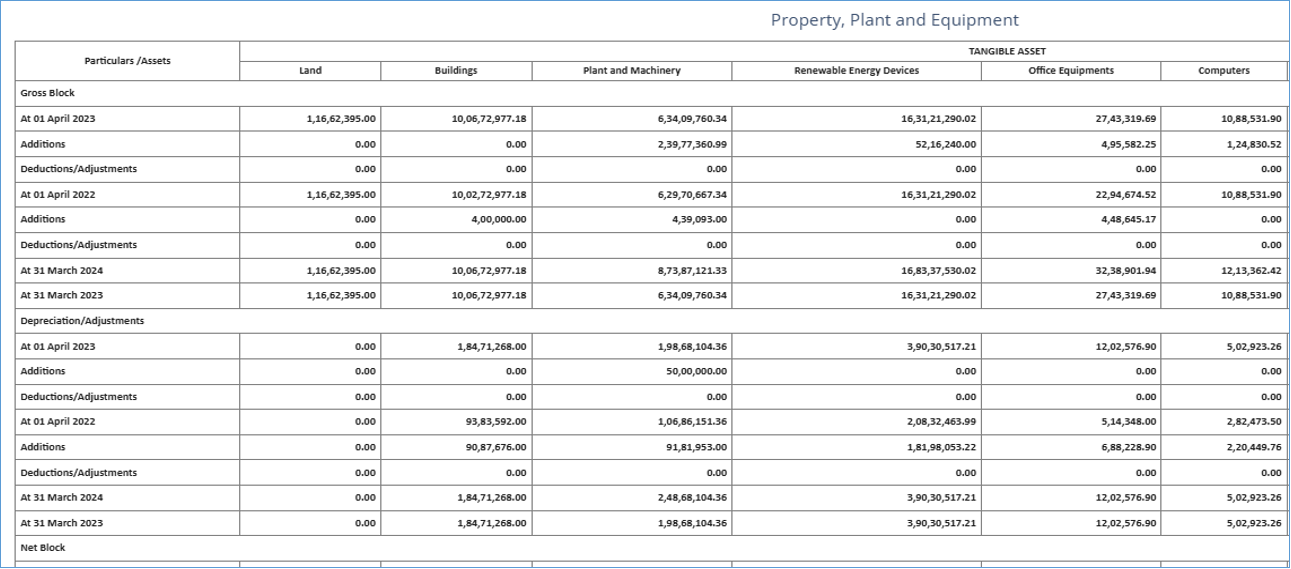

1.5 Tangible and Intangible Assets Schedule

Inclusion of previous year figures in Tangible and Intangible assets.